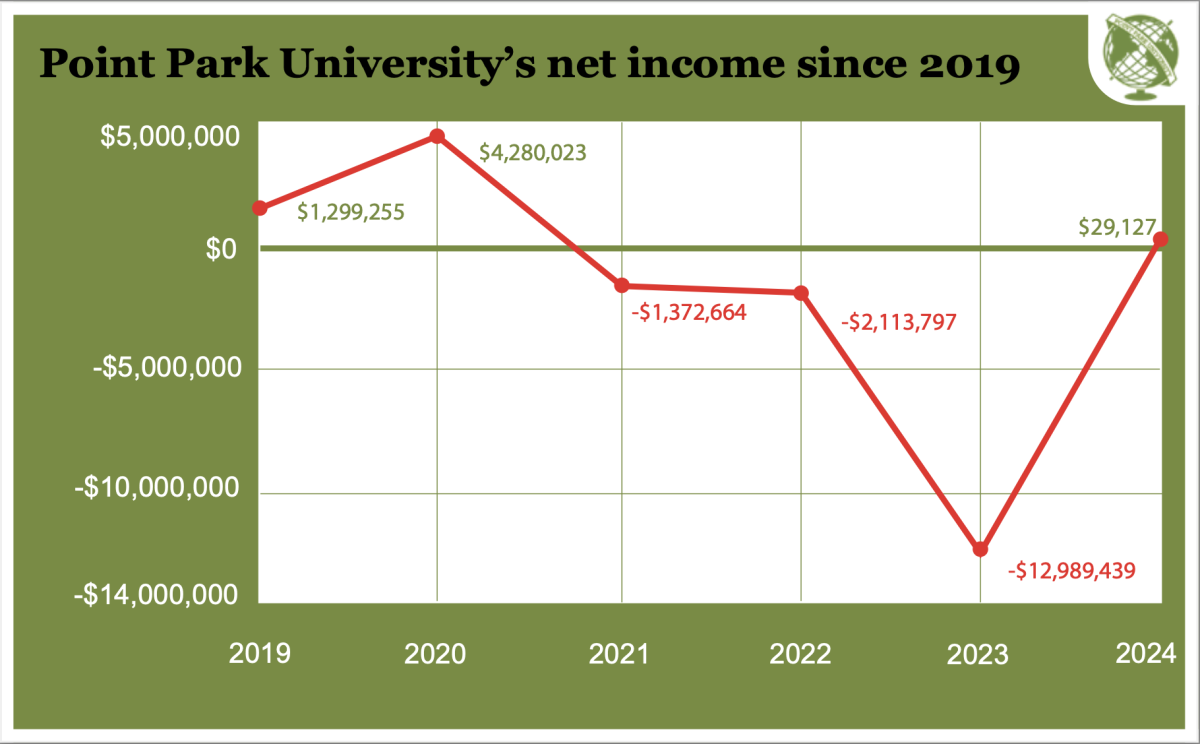

For the first time since 2021, Point Park University had a positive net income on its annual IRS Form 990, according to filings from August 2023 to August 2024 reviewed by The Globe.

Positive investments made the university about $12 million, which pulled it out of its accelerating post-COVID financial downturn.

The school lost nearly $13 million in its previous filings, which it attributed to lost enrollment in the wake of the COVID-19 pandemic.

Now, Point Park is the only university in Pittsburgh so far that did not report negative income.

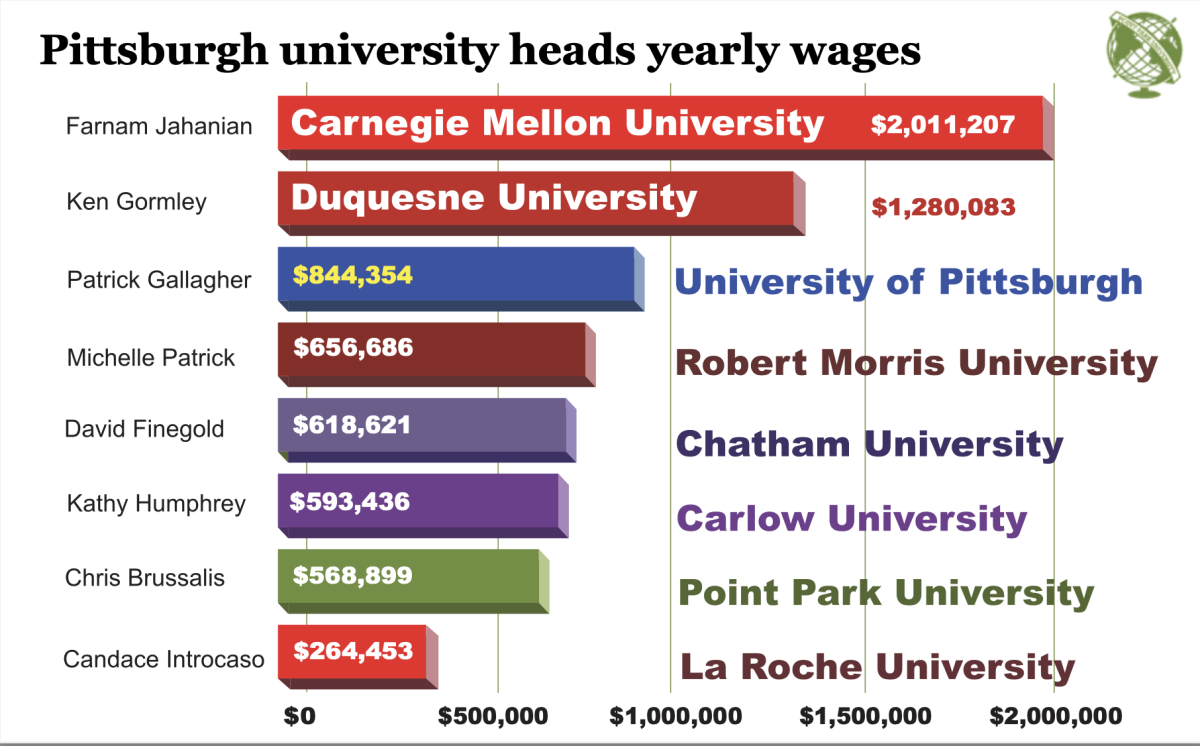

Carlow, Robert Morris and Duquesne University all reported losses in the same fiscal period. Other Pittsburgh universities, notably the University of Pittsburgh and Carnegie Mellon University, have not yet filed their annual Form 990.

President Chris Brussalis, while not elaborating on exact investments, gave credit to the Board of Trustee’s finance committee.

“We’ve been investing our money well,” Brussalis said. “We’ve been managing our portfolio well.”

Brussalis himself collected a $50,000 bonus, which brought his total compensation to almost $570,000.

That figure is based on more than just salary, though, and includes all forms of cash and non-cash benefits, such as health insurance. Brussalis was also the second-lowest compensated university head among Pittsburgh universities, according to each school’s most recent filings.

Brussalis attributed his and other faculty’s compensation figures to the work of a “national firm.” He did not specify who that firm was, but said they are hired by the university to benchmark faculty’s salaries, benefits and bonuses.

Former university presidents also showed up in the form. Paul Hennigan, who retired as president in 2021 — two years prior to the beginning of the fiscal period covered by the forms — was compensated about $324,000. And Don Green, who resigned from his post as president in January of 2023, received over $400,000 in compensation.

Both Brussalis and Lou Corsaro, the university’s assistant vice president of public relations, said these payments were due to deferred compensation packages agreed between the university and each respective past president.

Such forms of payment are not outright bonuses, but an amount of money earned by working and set aside for tax purposes, according to Brussalis, who said he will have the same arrangement when he retires.

“[Deferred compensation packages are] not unusual for a lot of industries,” Brussalis said.

Hennigan and Green’s respective compensation packages served as a key issue with the faculty union last year in their effort for a new collective bargaining agreement. University officials clarified that neither Hennigan nor Green should appear on next year’s filings.

The Globe did not reach out to Point Park’s faculty union for comment.

Karen McIntyre, a professor within the School of Education and former provost, made around $238,000, which makes her the highest compensated professor at Point Park.

The second and third-highest compensated were Darlene Marnich, a School of Education professor, and Dimitris Kraniou, a professor in the Rowland School of Business.

Marnich was compensated about $236,000 and Kraniou around $181,000.

“Executive” compensations, according to the filings, made up about $3.2 million — or 2.7% — of total university expenses. By comparison, other salaries and wages encompassed $35.9 million, or 27.4% of total expenses. 77 total employees were compensated over $100,000.

Bakertilly, a Pittsburgh-based accounting firm who independently audited Point Park’s tax forms, found what they said was a “significant deficiency” in internal controls that could potentially lead to misstatements in reported data.

That deficiency, according to both the audit and Jim Hardt, Point Park’s associate vice president of finance, was incorrectly formatted student loan data.

Point Park utilizes the National Student Clearinghouse (NSC) to transmit enrollment information to the National Student Loan Data System (NSLDS). Some students’ data, according to Hardt, did not follow the format recognized by NSLDS.

As a result, those students’ enrollment statuses were not updated in a timely manner, which was flagged in Bakertilly’s audit.

“The finding was labelled ‘significant deficiency’ as that is the standard language required by Single Audit standards,” Hardt said in an emailed statement. “The same language would be used even if only one student’s status was not updated timely.”

Corsaro added that the issue was corrected.